- Brussels is considering an outright ban on Russian fertiliser pushed by Finland and Sweden

- Trade bans introduced in 2022 caused global fertiliser and food prices to spike

- This could have serious consequences for palm yields and Indonesia’s fiscal position

Possibly the most overlooked story in trade and agriculture right now is about fertiliser. Specifically: The EU is all set to introduce new sanctions on fertiliser from Russia and Belarus.

The last time this happened was in 2022, and there was a global spike in fertiliser – and food – prices.

It was a massive disruption to global trade that had ramifications across the globe – and will have consequences for the palm oil and vegetable oil trade.

Europe’s Sanctions, Everyone Else’s Problem

The European Parliament and Council have adopted staged tariff measures targeting Russian and Belarusian fertilizer. Finland and Sweden have pushed the bloc to go further with a full ban. There will be a cap on Russian ammonia imports. If all this proceeds the impact will ripple through every fertilizer-dependent agricultural economy on earth.

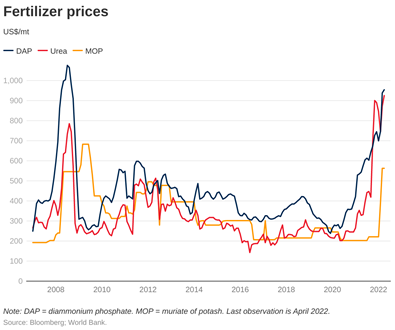

Why? Russia leads the world in nitrogen fertilizer exports and is the second-largest producer of phosphates and potash. In 2022, when the conflict began, fertilizer prices surged globally. The World Bank fertilizer price index captured the scale of the shock.

In West Africa, fertilizer prices effectively doubled. Some farmers reduced their cultivated area by 60%. Food prices spiked for populations already on the edge.

Indonesia was not spared. NPK prices basically doubled. For Indonesia this mean a massive allocation to fertiliser subsidies, When prices eased in 2023–2024, use recovered. But there was a clear point: when Europe’s political choices disrupt fertilizer markets, it is farmers in the Global South who pay the most.

Could it be different this time?

Europe’s problem at the moment is twofold.

First is that European farmers are struggling with high fertiliser prices from the Carbon Border Adjustment Mechanism (CBAM). COPA COGECA, Europe’s largest farm lobby last week pointed out that January fertiliser imports into the EU are 80 per cent below normal.

Second is that Brussels’ approach to agricultural productivity is often contradictory. At last week’s Munich Security Conference, Agriculture Commissioner Christophe Hansen spoke about increasing ‘weaponisation’ of food by Russia.

While there’s an understanding that they can’t be dependent upon Russia for energy, fertiliser and even food, there’s little motivation to actually improve agricultural productivity or lower agricultural costs.

Simultaneously, Companies such as Norway’s Yara see a Russian ban as an opportunity to gain market share in the European Union. Does this mean Brussels’ decisionmakers are asleep at the wheel? Or are they wilfully ignoring price rises?

The problem here is that the combination of CBAM, caps and sanctions will – as it did in 2022 – effectively bid up the price of fertiliser globally as the EU seeks non-Russian sources.

Jakarta’s Answer: Trade with Everyone

If Brussels hoped that its sanctions regime would isolate Russia from global commodity markets, Indonesia’s trade policy tells a different story.

In September 2025, the EU and Indonesia reached the substantive conclusion of the Indonesia-EU Comprehensive Economic Partnership Agreement (IEU-CEPA) — a deal that eliminates tariffs on over 98% of tariff lines and gives Indonesian palm oil improved access to the European market. Three months later, in December 2025, Indonesia signed a Free Trade Agreement with the Eurasian Economic Union — the Russia-led bloc that also includes Belarus, Kazakhstan, Armenia, and Kyrgyzstan. That agreement was signed in St. Petersburg, in the presence of President Putin.

The EAEU deal is not incidental to the fertilizer question. It is central to it. The agreement explicitly covers fertilizers among the products eligible for zero tariffs. The EAEU’s main exports to Indonesia include potassium fertilizer, the very input that is most critical for oil palm productivity. During the negotiations, Russia and Indonesia held bilateral discussions specifically on fertilizer cooperation, including fertilizer standards, import port regulations, and a potential joint-venture fertilizer factory. Russia’s Agriculture Minister discussed building a fertilizer plant in Indonesia during President Prabowo’s visit to St. Petersburg in June 2025.

Indonesia will trade with whoever serves its national interest. It will sign a trade deal with the EU in September and a trade deal with Russia in December. It does not share Europe’s geopolitical alignment and sees no contradiction in deepening commercial ties with both sides simultaneously. This is not unusual. It is standard practice for most developing countries. Europe’s security concerns do not automatically become the world’s trade policy.

This has direct implications for the fertilizer debate. If the EU imposes sanctions on Russian fertilizer, Indonesia has already built the institutional framework to maintain its fertilizer supply relationship with Russia.

But if global benchmark prices go up, no one is immune.

Indonesia’s Potash Vulnerability

Data from BPS-Statistics Indonesia show the country imported roughly 3.4 million tonnes of potassium chloride (MOP) in 2024. Russia and Belarus together supplied a substantial share, alongside Canada.

Nitrogen is less of a concern as Indonesia produces significant urea volumes domestically. Phosphate imports come largely from China and Vietnam. The critical vulnerability is potassium, and it runs directly through the oil palm sector.

When potash becomes expensive or hard to source, application rates fall — and yields follow. Research at Wageningen shows that nitrogen and potassium are the two dominant yield drivers. Where K is constrained, the penalties are significant.

Worse, oil palm biology involves lag effects. Reduced fertilization today depresses yields not just in the current season but across several subsequent harvest cycles. A single year of under-application echoes through the plantation for years.

The Numbers That Matter

If sanctions tighten potash trade the consequences for Indonesia are real. If subsidies aren’t in place, application could be cut. Large estates may cut K application by 10–20%. Smallholders may reduce application by 20–40%. Multi-year yield penalties could reach 3–8%.

A sustained 5% yield reduction implies 2–2.5 million tonnes of lost CPO. Indonesia accounts for more than half of global palm oil output. A loss of that scale would tighten global markets, increase substitution pressure on soybean and rapeseed oil, and push edible oil prices higher worldwide.

In other words, Europe’s fertilizer sanctions risk becoming a backdoor mechanism for global vegetable oil inflation paid for by consumers and farmers who had no say in the policy.

A Pattern of Indifference

There is a pattern here that developing countries recognize well. Europe makes policy decisions driven by its own political imperatives, with little regard for the consequences beyond its borders. The EU’s track record on palm oil, from the Renewable Energy Directive’s discriminatory treatment of palm-based biofuels, to the EUDR’s burdensome requirements on smallholders, to the copy-paste responses at WTO committee meeting, suggests that the interests of Global South producers are, at best, an afterthought.

Fertilizer sanctions would fit neatly into this pattern. The political benefits accrue in Brussels, Helsinki, and Stockholm. The costs are borne in Riau, South Sumatra, and West Kalimantan — by farmers who have no representation in European decision-making and no recourse when those decisions go wrong.